What Recessions Reveal About Property and Casualty Insurance Dynamics

What is a Recession?

A recession is commonly defined as a period of significant, broad-based decline in economic activity that lasts more than a few months. Recessions are indicated by falling real gross domestic product (GDP), lower income, rising unemployment and drops in industrial production and retail sales. In the United States, the National Bureau of Economic Research (NBER), a private non-profit organization, is considered the ultimate arbiter of when the U.S. economy is (or was) in recession.

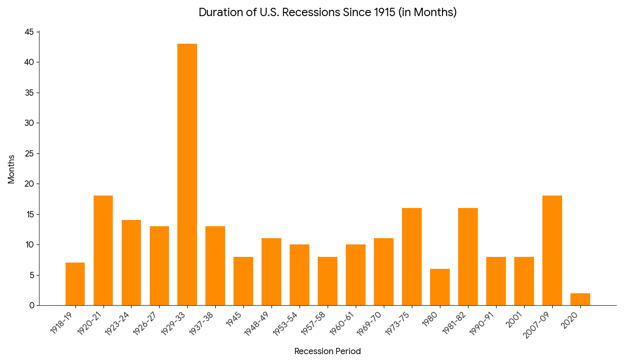

Historically, recessions occur every six to seven years, on average. The U.S. has experienced 34 recessions since 1857 according to the NBER, ranging in length from two months to more than five years. While the average recession has lasted 17 months, there are six recessions since 1980 that have lasted less than 10 months, reflecting changes in economic structure and policy responses. The question is: What are the indicators that best signal a recession in the property and casualty industry, and how do actuaries take these into account when setting reserves and pricing insurance?

Relationship Between Recession and Inflation

Inflation can serve as an early indicator of recessions, as persistently rising prices for goods and services over time often lead to a decrease in consumer purchasing power and slowed spending. A little inflation can indicate increased demand and higher profits. Uncontrolled high inflation, however, can have serious repercussions for economic growth if it surpasses the Federal Reserve’s target rate, currently around 2%. By examining historical patterns, periods of high inflation often led to a recession. The Oil Embargo recession from November 1973–March 1975 is an example. In contrast, the opposite is also true. The short COVID-19 recession caused a period of inflation in the years that followed.

Underwriting Indicators

Additional recession indicators emerge within the insurance industry through the underwriting cycle. Recessions are more likely to surface during hard market conditions, when insurers exit unprofitable lines of business or non-renew policies and tighten underwriting standards. Hard markets can also change how a company manages their investment portfolio, causing shifts toward more conservative strategies and diversified investments.

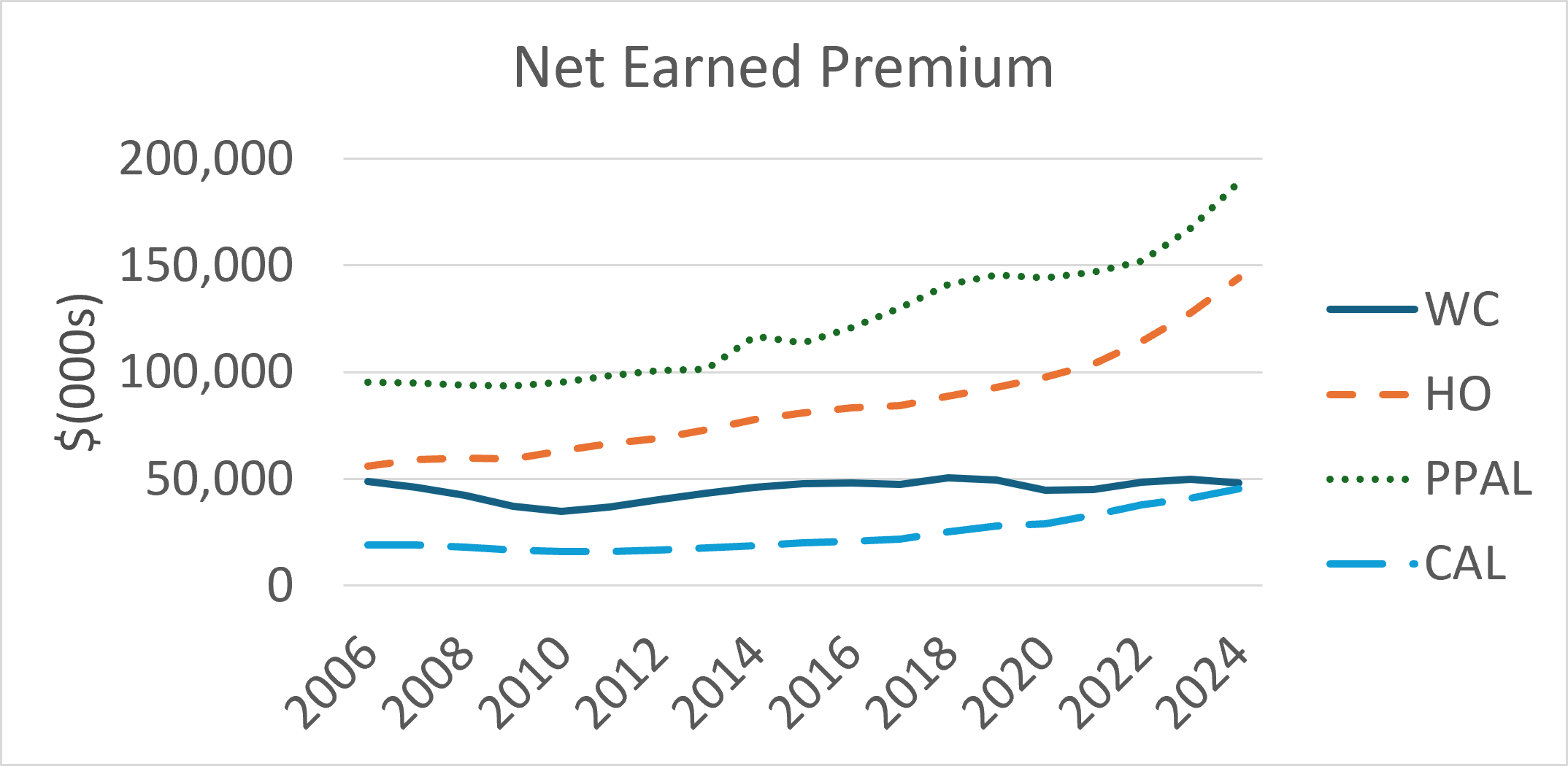

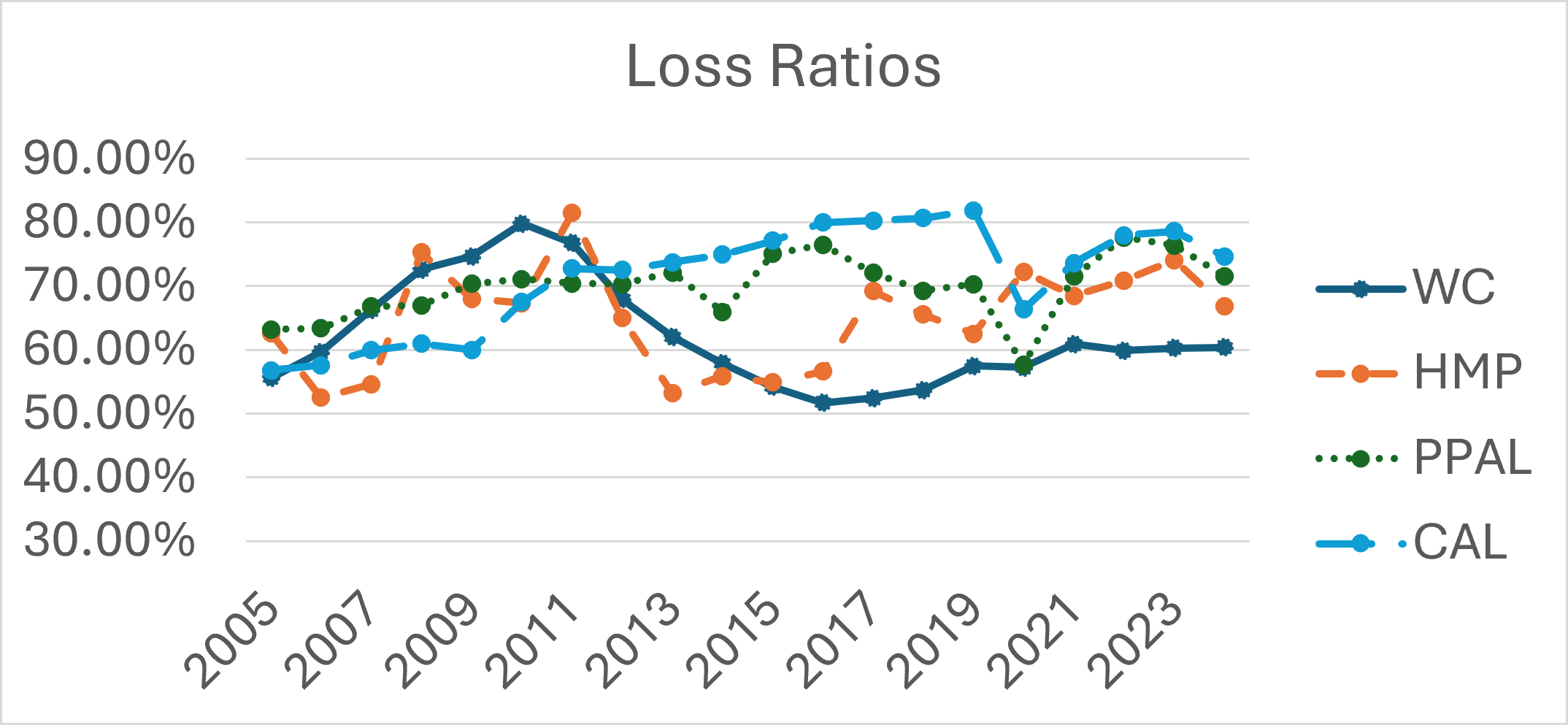

Net earned premium trends can also signal a recession. While premiums have tended to rise over time for most lines of business, workers compensation (WC) premiums have been more stable. Historical data showed noticeable declines in WC premium during the Great Recession and COVID-19 recession and loss ratios showed spikes during the Great Recession as well as reduced profitability. The absence of a spike during the COVID-19 period shows how distinct types of recessions affect different lines of business differently. Because WC is directly correlated to employment rate, it is often a more reliable recession indicator than other property and casualty (P&C) lines of business. Understanding these distinctions is essential for interpreting insurance-based recession signals and how the market may behave in the future.

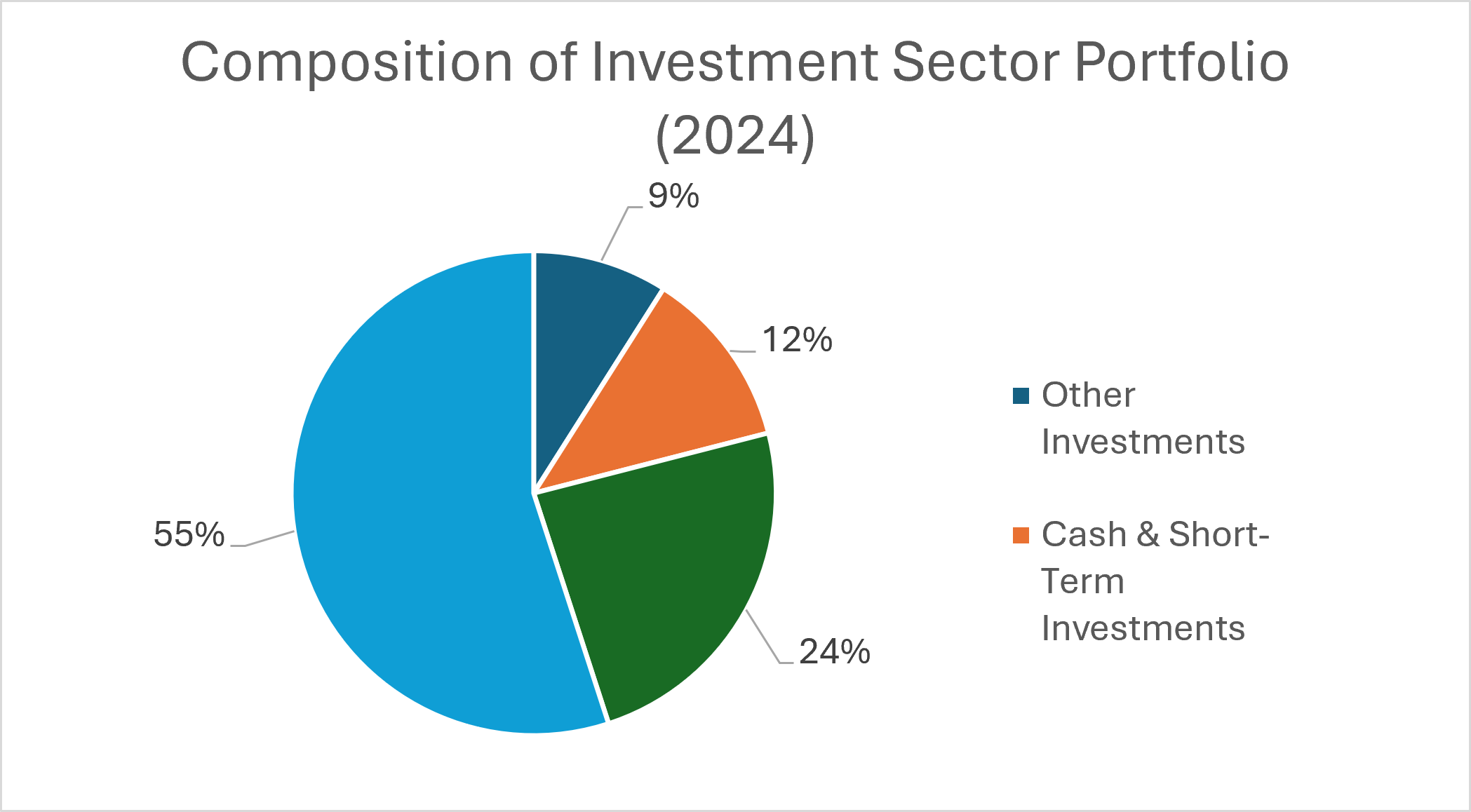

Overview of P&C Sector’s Investment Portfolio

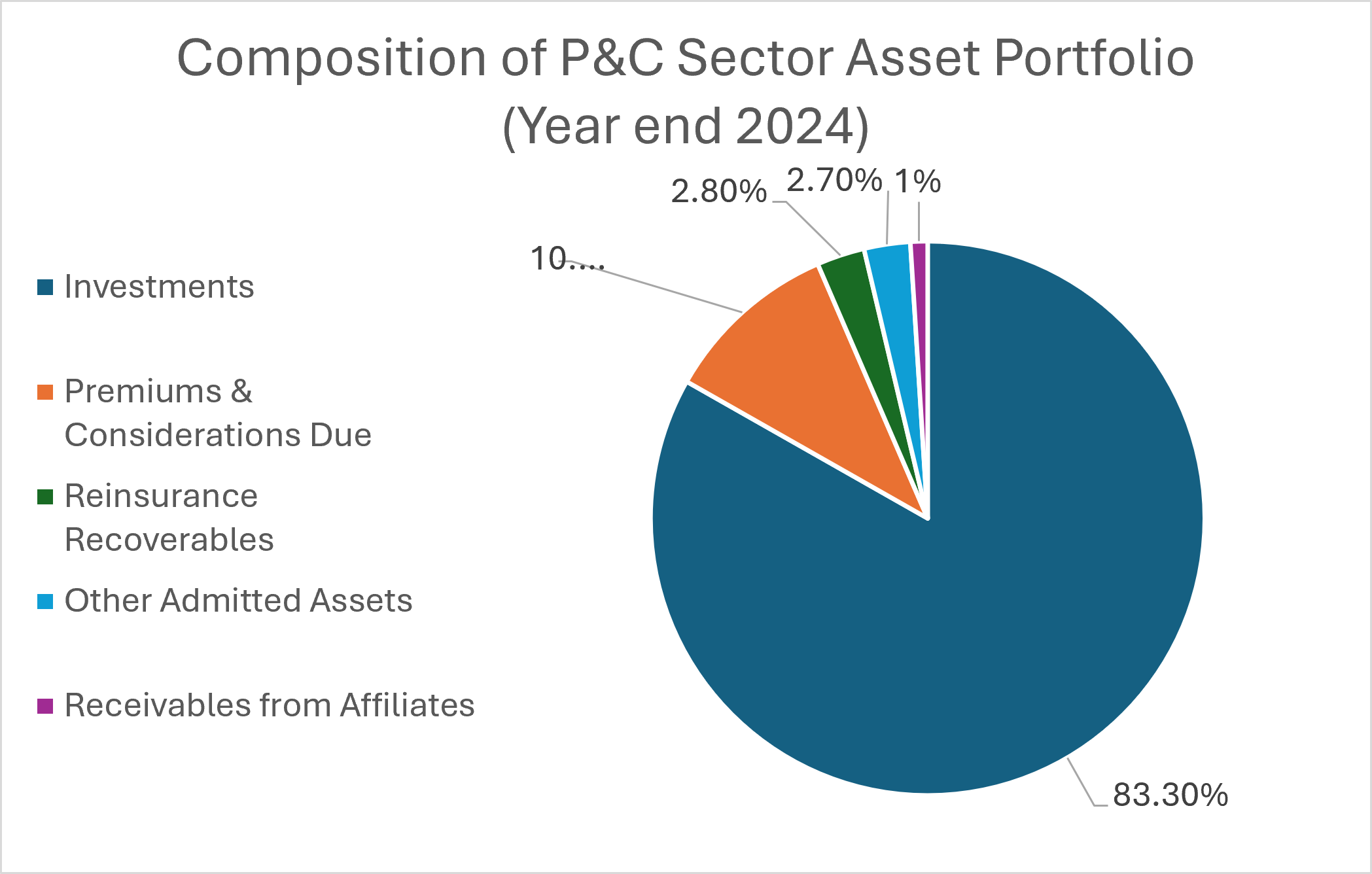

Like other sectors, investment portfolios of P&C companies play an important part in indicating recession and changes in corporate investment strategies. As of year-end 2024, investments comprise approximately 83% of total assets in the P&C sector, which highlights the industry's heavy reliance on investment market performance. The investment strategy for the P&C sector has remained steady over the last decade, with long-term bonds accounting for 55% of the portfolio, followed by common stocks at 24%. Combined, these two categories account for nearly 80% of all invested assets, creating a foundation that prioritizes fixed-income stability while maintaining significant exposure to equity markets.

Investment Market Performance During Recession

Market crashes tend to go together with recessions. For instance, during the COVID-19 recession, the S&P 500 and NASDAQ dropped by 34% and 30%, respectively. In recessionary periods, P&C insurers can face sharp declines in equity valuations and reductions in dividend income (Song, 2022). Research by Tim A. Kroenke in 2022 stated that real dividends, the purchasing power of dividends, fall by an average of 13% within the first four quarters after the beginning of recessions (Kroencke, 2022).

When the economy enters a recession, the Federal Reserve typically responds by lowering interest rates. This causes the price of investment bonds (corporate and governmental) to rise. While longer-term company bonds often perform well during these periods due to appreciation in bond value, the P&C sector’s "laddered" portfolio approach or spreading bond investments across multiple maturity dates introduces unique challenges. As their portfolio’s higher-yield bonds mature, insurers reinvest that investment cash into new bonds with significantly lower interest income. Furthermore, corporate bonds, the largest bond investment for the sector, carry credit risk and default probabilities that are higher during an economic downturn. The risk is compounded by liquidity concerns, as transaction costs rise and dealers shift from buying to selling, making it harder to exit investment positions efficiently.

Pricing and Reserving Considerations

In his article “Underwriting Cycles and Business Strategies, Sholom Feldblum states that “Actuaries Indicate Rates, but the market sets prices.” That observation highlights critical discipline actuaries need to follow to avoid being overactive to short-term market conditions (Feldblum, 1990).

The inherent lag between when data is collected and analyzed and implemented in rates requires that actuaries must take a measured approach. Although higher inflation and recessions do not always occur together, actuaries must still account for elevated inflation. That includes social inflation and nuclear verdicts, as well as general inflationary price increases when pricing insurance products.

Proforma financial analyses that stress test new captives or companies become extremely important during periods of market uncertainty. Such analyses allow the organization and the actuary to better anticipate potential shifts in economic conditions and ensure the company does not become insolvent by assessing proper investment strategies and up-front capitalization.

These considerations extend beyond pricing into reserving as well. Recessions can lead to increases in fraudulent claims, shifts in claim severity, or high medical liability and litigation costs driven by both social and general inflation. Understanding the characteristics of a line of business, short tailed or long tailed, is essential for setting appropriate and adequate reserves. Tools such as IRIS ratios can help assess a company’s solvency, with IRIS ratios 11-13 (one year reserve development, two-year reserve development, and estimated current reserve deficiency) being especially relevant to evaluating reserve adequacy and liquidity. These practices help actuaries understand financial stability across varying economic environments.

Understanding how recessions unfold is not just an academic exercise for actuaries. It’s a core competency that shapes a company’s financial judgement. By recognizing how recessions influence investment portfolios, capitalization, and overall solvency, actuaries are better equipped to set adequate and reasonable reserves and protect long-term financial stability. This awareness strengthens and supports the company, ensuring that policyholders and stakeholders remain secure even when the economic conditions are at their most uncertain.

Citations

Feldblum, S. (1990). Underwriting cycles and business strategies. Proceedings of the Casualty Actuarial Society, 77, 175–235. https://www.casact.org/sites/default/files/old/01pcas_feldblum.pdf

Kroencke, T. A. (2022). Recessions and the stock market. Journal of Monetary Economics, 131, 29–47. https://doi.org/10.1016/j.jmoneco.2022.07.004

Song, R., Shu, M., & Zhu, W. (2022). The 2020 global stock market crash: Endogenous or exogenous? Physica A: Statistical Mechanics and Its Applications, 585, 126425. https://doi.org/10.1016/j.physa.2021.126425

U.S. Department of the Treasury, Federal Insurance Office. (2025, September). Annual report on the insurance industry. https://home.treasury.gov/system/files/311/Final%20FIO%202025%20Annual%20Report.pdf

News & Insights

How the Insurance Industry is Navigating the Complex Debate Over Fairness in Pricing

Keeping It Clean: Understanding Pollution Liability Insurance and Its Future

Not Another AI Panel: Notes from the Bermuda Captive Conference